A Risk Parity Transition Case Study: Nolan

Cool case study for transitioning a fantastic "VTSAX and Chill" portfolio for accumulation into a diversified, resilient portfolio for decumulation, or in other words, "Risk Parity and Roll."

Back in mid-October, I wrote a post about how to transition a portfolio as retirement approaches. At the very end, I floated a small experiment: if anyone wanted to submit their own situation, I’d walk through how I’d think about transitioning their portfolio—out loud and in public.

The idea was a simple win-win: They’d get a thoughtful, end-to-end analysis; readers would get to see the reasoning process in action.

A few weeks ago, a reader named Nolan took me up on it.

Nolan wrote to say that while he feels he’s in a strong position, he’s unsure whether his current portfolio is the right portfolio for the next phase of his life. Specifically, he wanted to explore three questions:

How should his portfolio change as he approaches retirement?

What withdrawal rate could he reasonably target?

What’s the right order of operations—both before and after retiring?

Let’s get into it!

The Setup: Nolan’s Situation

Here’s the relevant background:

Nolan is 44, married, no children

Single-income household, government job

Target retirement age: 50

Does not own a primary residence (yet?); location in retirement undecided

Saves roughly $60,000 per year across TSP, Roth IRA, and taxable brokerage

Retirement spending target: at least $100,000 per year

Government pension expected to provide ~$60,000/year after tax, inflation-adjusted

Open to part-time work in retirement

Nolan currently has just under $2 million invested. You can see the full account of his current holdings on this spreadsheet in the “List of Assets” tab, but in general, his portfolio is essentially a classic accumulation portfolio that would make JL Collins proud:

45% in total US Equities

28% in the S&P 500

5% in US Mid-Caps

3% in US Small-Caps

19% in International Developed equities.

How Nolan’s Current Portfolio Has Performed

Using data back to late 1979 (to allow apples-to-apples comparison later), Nolan’s portfolio shows excellent performance—exactly what you’d want during accumulation:

If Nolan simply keeps contributing for six more years and earns a conservative 7% return, his portfolio would be worth ~$3.4 million by 2032. That’s a wonderful position to be in at age 50, and it reflects a lot of good decisions. Nice job!

But strong accumulation performance doesn’t automatically translate into a good decumulation portfolio.

Why This Portfolio Starts to Break Down Near Retirement

The issue with Nolan’s portfolio isn’t returns—it’s risk.

A portfolio that can lose more than half its value, even temporarily, is manageable when you’re accumulating and ignoring the noise. It’s much harder to live with when you’re relying on it for income.

That volatility of Nolan’s current portfolio shows up directly in the math surrounding withdrawals.

Using a 25-year rolling window, Nolan’s current portfolio would have:

Perpetual Withdrawal Rate (100% success): 2.7%

Safe Withdrawal Rate (100% success): 4.3%

Those aren’t very high numbers. Despite its impressive growth overall, Nolan’s current portfolio isn’t particularly generous when it comes time to spend from it as its volatility leaves it susceptible to huge drawdowns that could strike exactly when Nolan needs to withdraw from it, exacerbating the pain. This is a textbook case of why I consider withdrawal stats as important as Compounded Annual Growth Rate.

Nolan has borne a lot of market risk and already won the game. There’s no need to keep playing the same way.

How I’d “Risk-Pari-fy” Nolan’s Portfolio

Nolan is actually in a uniquely strong position to adopt a Risk Parity-style portfolio on the higher end of the risk-taking spectrum:

His government pension provides a lifelong, inflation-adjusted income floor

He has no strong legacy requirement

His goal is stability and flexibility, not maximizing terminal wealth

Risk Parity portfolios generally have between 40 and 60% in equities. Given Nolan’s pension buffer, I’m comfortable toward the higher end—but there’s little benefit in going beyond that.

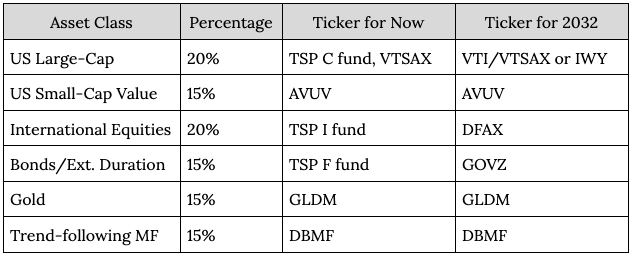

I settled on 55% equities, split as follows:

20% U.S. large-cap

20% international equities

15% U.S. small-cap value

The remaining 45% is split evenly among diversifiers:

Extended-duration Treasuries, to protect against recessions.

Gold, to offset debasement risk.

Trend-following managed futures, to try to survive during stagflation.

In terms of ticker symbols, Nolan doesn’t have the widest of choices now, though he will once he moves the TSP to a traditional IRA when he retires. The following chart thus lists possibilities for now and for post-retirement for what I am calling “Nolan’s Risk Parity Portfolio”:

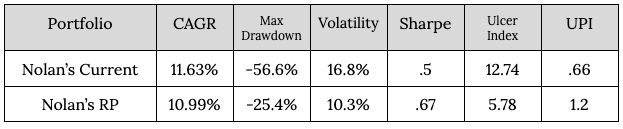

This produces a portfolio with slightly lower returns—but dramatically better stability. Looking at the 46 years I can backtest, you’ll see it compares very favorably to his current portfolio:

That’s the trade-off Risk Parity makes: give up upside to massively reduce downside stress. For retirement, that’s a good deal.

What Could Nolan Safely Withdraw?

This is where the Risk Parity portfolio really shines.

Using a 25-year rolling window, Nolan could withdraw the following percentages from his nest egg if he were to adopt the Risk Parity portfolio (and if the future were more or less like the past!):

If you want a number that would have survived 100% of the rolling 25 year periods in the backtest: PWR : 5.24% or SWR: 7.2%.

If you want the number that survived 90% of the periods in the backtest: PWR: 5.88% or SWR: 7.62%

I argued recently that PWR was the best number to focus on, but given Nolan’s pension and flexibility, I actually think SWR is the more appropriate constraint for him. He doesn’t need to preserve capital indefinitely, and he has buffers most retirees don’t.

To narrow in on a withdrawal rate, let’s take some number in the middle of the range between 5.24 and 7.62%. I think 7% is plausible and 6.5% is comfortable, but if this were me…

I’d go with 6% as my baseline annual figure.

For a $3.4 million portfolio, that’s ~$200,000 per year, before the pension. You can see the different withdrawal rates and how much money they’d be on the spreadsheet in the bottom left.

Nolan worried about “eking out” $40k, but it’s clear that there really is no need to eke. The data suggests his modest goals are undershooting his likely reality by a wide margin. Keep in mind that in every single calculation so far, I have erred on the side of caution when given the choice.

The Order of Operations

Nolan’s situation is enviable. He’s done such a good job preparing for retirement that his standard of living isn’t just maintained in retirement - it actually jumps.

The practical steps for withdrawing this amount for Nolan to make it all happen are not quite as enviable, though, since the location of where the money is now puts some constraints on how to change his portfolio now and over the next six years.

Right Now

There’s some major adjusting to be done within the Roth portfolio and some minor adjusting in the TSP. The Roth is valuable real estate and normally, I wouldn’t recommend owning any gold within it. Gold doesn’t produce distributions and, despite recent performance, it typically is not a source of high returns. For that matter, trend-following managed futures aren’t great for a Roth, either.

But here we conflict with another principle of mine - I don’t recommend generating taxable events in order to transition a portfolio. In this case, it would be great to reduce exposure to the S&P by cutting out VTSAX in the brokerage account, but that can’t be done without a huge tax bill, so we’re left with moving things around in the Roth.

It is easy to move things around in the TSP, but there, Nolan is limited by the fund choices. So, the over-exposure to US equities there can’t really be dealt with, and there aren’t great alternatives for the other elements.

As for the brokerage account, I’d advocate not really doing much with it, other than refrain from putting any more into VTSAX. To be honest, Nolan doesn’t even really need to contribute what he is currently into the brokerage account to be just fine - that money could be spent on some awesome vacations instead.

So, starting today…

In the TSP, take $300,000 out of C Fund, and add $100,000 to the I fund and $200,000 to the F Fund.

In the Roth, I’d sell all (yes, all) of the holdings in VTSAX, which would be around $430,000 and then put $150k each into GLDM and DBMF, with the remainder going into AVUV.

In the brokerage account, I wouldn’t touch anything for now.

Then, over the next six years, I’d try to get towards those ideal percentages as best I could, but without selling anything that would trigger a taxable event. It is unlikely that following the steps here would get Nolan to the ideal proportions by 2032, but it will get the portfolio moving in the right direction.

If any holdings of VTSAX in the brokerage account were to drop below their cost basis, I would sell them at that point. Nolan should be careful, though, of claiming losses on VTSAX in the brokerage account but buying additional shares of VTSAX or a substantially similar fund around the same time somewhere else, even as a dividend reinvestment. Such a move would violate “wash sale” restrictions.

Over the next six years…

In the TSP, I’d split future contributions between the I fund and the F fund.

I’d put future Roth contributions into AVUV.

In the brokerage account, I’d direct future contributions into whatever fund among AVUV, GLDM and DBMF were the farthest away from its ideal percentage.

Fast forwarding to 2032, when Nolan is ready to retire, the first order of business would be to rollover the TSP into a traditional IRA. It’s impossible to give percentages or dollar amounts, but generally speaking:

then in 2032…

In the new rolled-over TSP/IRA, purchase GOVZ, DBMF and GLDM so that they each became 15% of the total portfolio.

Positions in AVUV and DFAX could also be increased so that each represented 15% or 20%, respectively.

I can’t imagine much would need to be put into US Large-Cap because the huge chunk in the brokerage account would still be there, but if not, then try to get US Large-Cap to 20%.

If optimization were the goal and one were willing to take the time to do a lot of asset swaps, the most efficient way forward would be to have all of GOVZ, GLDM and DBMF in the traditional, and leave the Roth for AVUV, DFAX and then whatever was needed to fill out the US Large-cap allocation.

…and then after 2032…

The tricky problem left is how to draw from the various accounts in the right order. For this, actually, I would recommend Nolan hire a fee-only CFP or a tax specialist to go through the possibilities - money spent on that type of advice would be well worth it. I certainly have my thoughts, but this is definitely an area in which professional advice should be sought and followed.

With that said, the general plan would be to take from the brokerage account first until age 59½. Looking at the account, there may be enough in VTSAX to allow for that, and a backup could be to withdraw contributions made into the Roth IRA. It’d be much better not to do so, but that’s an option. At age 60, Nolan gains flexibility since there would be no more early withdrawal penalties. All things being equal, it’d be better to take from the traditional first, but there are other factors that a professional could advise Nolan on.

Wrapping Up

Nolan’s in a great situation, but I would recommend some pretty big shifts to take risk off the table. His accumulation strategy was exactly right for getting him here. But a more resilient, diversified portfolio gives him something different going forward: confidence, flexibility, and peace of mind.

Exactly what Risk Parity is really for.

Really good write up. I’m just curious why 401k’s 403’s etc can’t be rolled to an IRA while working especially the portion that you’ve contributed over the years? I know it’s the rule most places, but any insights as to why? I think situations like this will grow increasingly common due to the strong stock market returns and the increasing understanding of portfolio diversification through alternatives not to mention gold being on a tear. More and more investors are going to be seeking these alternatives and finding their 401k’s don’t offer them. Then it almost begs the question is it worth separating from your job to be able to roll the investments to an IRA. Hats off to Nolan, something I wish all middle and high school students were exposed to was more stories like this.