Portfolio Breakdown: The Equity Triangle

If you're still years away from retirement, Risk Parity may not be the right tool for the job. The Equity Triangle offers a simpler path: growth, balance, & almost no maintenance.

When you seize upon an idea like I have sized on risk parity, one of the easiest traps to fall into is to become the hammer that sees everything as a nail.

In writing all about RP, I have focused on cases where a hammer is indeed the right tool for the job. For questions about portfolios leading up to and then in retirement, when the objective is how to manage decumulation, yes, Risk Parity is the best investment framework out there. You can’t beat Risk Parity if the goal is to build stable portfolios that prioritize PWRs over CAGRs.

But what about everyone else? What about the investor in their 20s, 30s, or 40s who is simply trying to build wealth? What about the accumulation stage, when you’re not even thinking yet about withdrawal rates?

For them, my answer is much simpler: The Equity Triangle.

Of all the portfolios I track, this is the one I’d feel most comfortable recommending to the average investor in the accumulation phase. It’s simple, globally diversified, low-maintenance, and built around the idea that you don’t need complexity to be successful.

The Portfolio

The Equity Triangle is simply:

That’s it.

This is a very simple 2:1, US to non-US split, roughly aligning with global stock weight. US stocks account for roughly 60% of global market capitalization, while international stocks make up about 40%. This portfolio isn’t perfectly aligned, but it’s close enough without introducing unnecessary complexity.

Within the US allocation, the portfolio uses an “equity barbell”: growth on one side, value on the other. Growth and value tend to take turns outperforming. Nobody knows which will dominate over the next decade, so owning both is a simple way to avoid making a prediction.

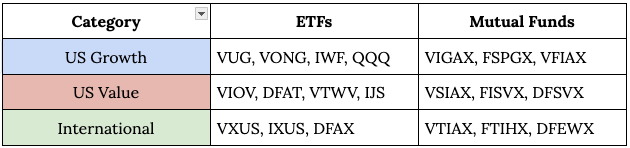

Fund Choices

One thing I like about this portfolio is that almost every brokerage account, IRA, pension plan, or 401(k) offers suitable building blocks.

If I had the world of funds to choose from, I’d use:

If those aren’t available, there are plenty of perfectly good alternatives.

Don’t overthink this part. The exact ticker matters far less than most investors believe. If you get stuck, go to your favorite AI engine, copy and paste what is available, copy and paste this section, and ask it to recommend funds. Easy peezy.

Managing the Portfolio

The beauty of the Equity Triangle is that it practically runs itself. Start initially with one-third in each, and then…

…in a tax-deferred account, like a 401(k) or IRA…

If new contributions are automated, then direct them equally

When contributions are occasional, then direct them to what’s lowest

Rebalance once per year by selling what’s high and buying what’s low within the account to maintain balance.

If you miss a year of rebalancing, don’t lose sleep over it.

…in other accounts…

Handle new contributions as above, depending on whether they are automated or not.

But, don’t sell anything just to maintain balance, since this will trigger taxes.

Yes, one-third of your portfolio in each part of the triangle is the goal, but it is not a big deal if its a bit off from that. Just do your best.

Dealing with Volatility

One thing to understand: this is still a 100% equity portfolio. That means it will be volatile, and there will be years when it falls 20%, 30%, or more.

My advice for dealing with those periods comes from an unexpected source: Raiders of the Lost Ark. When Indiana Jones was there for the opening of the Ark of the Covenant, he survived the demons and phantasms by keeping his eyes shut.

Investing in the accumulation stage can be similar. When markets inevitably get ugly, just don’t look at them. Instead, just keep buying.

Performance

The Equity Triangle wasn’t cherry picked, or settled on by searching for the equity funds with the highest historical returns, and I really can’t promise that this will be the best 100% equity fund you can hold. I don’t know that.

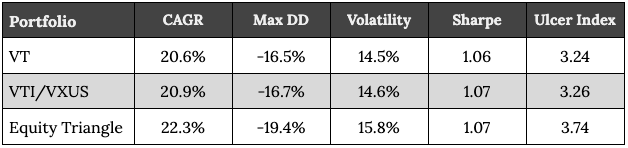

Still, based on historical performance, it has been fine compared to two other simple, all equity portfolios: one with 100% in VT, and one that is 2:1 VTI and VXUS.

If I use the exact ticker symbols in my ideal version of the Equity Triangle, I don’t get that long of a backtest due to the youth of AVNV — just three years:

I get slight over-performance with the Equity Triangle compared to the others, though with a little bit higher volatility, as well.

I can do a little finagling, substituting out my specific fund choices with some similar ones, to get the backtest back to 2005 (for the record, VIGAX for IWY, DFSVX for AVUV, and DFIEX for AVNV). The results once again are bunched, with ever-so-slightly better returns and ever-so-slightly higher volatility for the Equity Triangle.

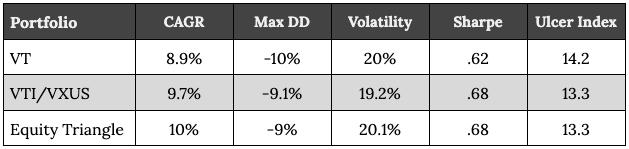

How Has It Done in Real Time?

I have also been tracking the Equity Triangle in the wild as part of my test portfolio series, and specifically, how well it can withstand a 4% withdrawal rate.

Among the RPC test portfolios, the Equity Triangle sat in fourth place as of May 2026. Only Shannon’s 50/50 and two leveraged Risk Parity portfolios—the RPC Hare and the Tall Stack—were ahead of it.

That makes sense. A 100% equity portfolio should be aggressive. It just won’t keep pace with portfolios using leverage to achieve even greater stock exposure.

Even so, the results have been impressive, with approximately 16.1% CAGR even after accounting for withdrawals.

My Recommendation

This is the portfolio I’d recommend to most investors during the accumulation phase. Not because it’s perfect, but because it’s practical. The Equity Triangle:

has strong long-term growth potential

has broad variety within equities (though no diversification beyond that!)

is easy to explain and easy to start

has minimal maintenance requirements

Now would I personally use it? Probably not.

I’d add capital-efficient ETFs such as RSST and RSSB, sprinkle in some leverage through UPRO and CAOS, and use a more sophisticated rebalancing process to harvest additional diversification benefits. In other words, I’d go with the RPC Hare.

But that’s not what most people need. Instead, they need a portfolio they can understand, stick with, and keep funding year after year. For that purpose, the Equity Triangle is hard to beat.

My general path towards retirement would be:

Use the Equity Triangle until you’re about ten years from retirement.

Then begin learning about Risk Parity, diversification, and decumulation portfolios.

Start buying those diversifying asset classes not in the Equity Triangle, such as long-term bonds, trend-following managed futures, and gold.

Within a 401k or IRA, gradually start the transition toward a retirement-focused portfolio such as the RPC Tortoise, Short Stack, or the Golden Butterfly.

Until then?

Put one-third into each sleeve, keep contributing, rebalance occasionally, and spend your time thinking about things other than your portfolio.

The thing I like about the equity triangle is that it is accessible. Since most folks do a lot of their accumulation in employer sponsored plans, they won't have the option to do something like the 10X10 Hare. but most plans have Growth, Value and International funds to choose from.

A few years back, when my daughter got her first employer sponsored plan, I set her up with something similar: 40% SP500, 30% Value (split evenly between Large and Small), and 30% intl total market. This mix has ROCKED for her the past 4 years. She is up nearly 13% YTD.

Looking forward to the piece on Momentum. Having played a bit in testfolio it seems Momentum vs Growth adds higher return, higher sharpe ratio, but higher drawdowns and higher ulcer index. Better performance but a a bumpier ride. Which is consistent wth how Larry Swedroe described Momentum in his book on factor investing ie there is a persistent Momentum premium but it is subject to sharp reversals. This is just looking at the equity sleeve, one will likely have other diversifiers in drawdown. But it does suggest that at least in accumulation mode where you can ride out the bumps it might be worth considering.